Making College Affordable: Providing Low-Income Students with the Knowledge and Resources Needed to Pay for College

Clarifying Financial Information

The federal government has recognized that students have the right to data that can help them make the best decision regarding their education.³ Colleges thus make a range of information available to students, such as the price of attendance, graduation rates, and student body diversity. However, this information is disseminated in various ways that are not always the most user-friendly for the individual student. Some facts are distributed to all enrolled and prospective students or are available online to everyone, while others are available only upon request, or sent out in publications and mailings. Sadly, the information provided is often a confusing mess, and low-income students — often sorting through the data without a seasoned counselor at their side — must navigate these puzzles on their own.

Information that is only available upon request or through selected mailings puts low-income students at a disadvantage. Students may not be aware that the data even exist, much less that they should be seeking these figures. Lack of understandable information puts low-income students at a disadvantage, and they may incorrectly conclude that a college education is simply unattainable or may enter college without a full understanding of how to navigate the many financial aid programs, and ultimately drop out.

Schools should transparently provide all students with the relevant knowledge needed to make the best decisions about their education and paying for it. Schools can proactively support low-income students by providing clear, comprehensive information to all students, regardless of whether it is requested. This includes providing students with the most accurate figures available related to costs, financial aid, and student success, as outlined in our first five strategies below.

Strategy 1: Clarify financial aid letters

Accompanying many offers of admission is a financial aid award letter. These letters often use acronyms and abbreviations, and they may lump together scholarships and loans in ways that are difficult for students and families to understand.⁴ Variation in financial aid letters from school to school can make it difficult for students and families to compare offers.⁵

To address these issues and help families make more informed decisions about college, the U.S. Department of Education and the Consumer Financial Protection Bureau developed the “Financial Aid Shopping Sheet” in 2012. This form was designed to simplify information regarding cost and financial aid and allow students to easily compare institutions. Elements of this form include:

- Separation of loans from grants and scholarships.

- A concise statement that grants and scholarships are gifts that do not need to be paid back.

- The sources of grants and scholarships.

- The net (“actual”) cost of one year’s tuition.

- Clear language (e.g., no abbreviations or acronyms).

In an open letter to college and university presidents, the Department of Education asked institutions to adopt this form for the 2013–14 school year. As of January 2017, 3,278 institutions — including 60 selective institutions — have obliged.⁶ A copy of the form and a list of participating schools can be found on the U.S. Department of Education website. More schools are using this form every year. Schools should at the very least use it as a template to clarify the elements of their financial aid so students can compare offers.

Institutional award letters should make clear:

- The amount of grant aid the student is receiving, with clear language indicating that grants are gifts that do not need to be paid back.

- The source of each grant.

- Possible additional sources of funding (e.g., private scholarships) to pay the net cost (the difference between cost of attendance and grant aid).

- Clarification that loan amounts are suggestions, not requirements.

- A clear statement of how much money the student and family will need to pay, including an explicit statement that loans must be repaid.

- The net cost of attendance.

In addition, schools should make clear the terms of continuation of any aid:

- The requirements for maintaining each form of grant funding, such as grade point average requirements or minimum credit load requirements.

- A disclosure as to which grants must be renewed annually (including federal or state aid) with instructions on how to renew the aid.

Strategy 2: Provide students with a four-year estimate of expected costs

Unexpected rises in tuition can derail students, particularly those who may already be struggling financially to stay in school. Simply informing potential students that tuition prices may increase is not sufficient. While schools cannot be expected to know the exact tuition costs of future years, schools can project potential increases in tuition to help students make informed decisions and prepare for the next four to six years. Giving students an idea of the price of education for the duration of their schooling can allow students to budget and plan for potential tuition increases well in advance. Some schools have begun offering this information on their financial aid websites. Other schools can adopt these best practices:

- Towson University projects four-year university costs for fall 2017 through 2020.

- Manhattan School of Music provides estimated projected cost of attendance for 2017–18 through 2021–22.

- Culver–Stockton College provides estimated annual costs for the 2018–19 and 2019–20 school years.

- As of Fall 2017, several schools provide cost of attendance for the 2017–18 and 2018–19 academic years. For example, Sweet Briar College and Wesleyan College both provide data on two years of tuition and other costs.

Supplying future cost estimates is useful for students as they explore various colleges. An optimal solution would be a calculator that could estimate each individual student’s potential net cost (incorporating financial aid) over the course of college.

Strategy 3: Establish clear policies regarding financial aid eligibility requirements

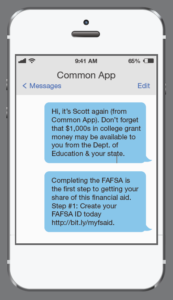

Figure 1: FAFSA Text Reminder from the Common App. Source: “Using Texts to ‘Nudge’ Students on Financial Aid,” Education Week, October 11, 2016.

Most students who lose their eligibility for student financial aid do so because they lack the necessary grades, and therefore are unable to meet the “satisfactory academic progress” requirements of their aid program.⁷ Under the Student Right-to-Know Act, schools must make the conditions of satisfactory academic progress “available” to all benefit recipients.⁸ However, schools can meet the requirements of the statute in a number of ways. The most direct way would be by including these requirements in the same envelope with their financial aid award letters, but not all schools choose this option. Instead, schools frequently make this information available through publications or online.

Once students are enrolled, institutions should remind them periodically of requirements and deadlines. The Free Application for Federal Student Aid (FAFSA) form is a requirement for the Pell Grant, the federal government’s program for the most financially-strapped students, and for a number of other public and private scholarships. FAFSA completion is important for maintaining various forms of aid. Students are not always aware that FAFSA must be completed annually in order to continue receiving need-based aid. Schools should remind students of specific FAFSA deadlines. Research suggests that low-cost interventions, such as text reminders, improve students’ completion of FAFSA and other college related tasks.⁹ Many schools already communicate important information, such as emergencies, to students through email, text, and automated messages (Figure 1). Transmitting reminders about financial aid deadlines would benefit many who would otherwise drop out.

? Schools Offering Financial Aid Text Notifications

Strategy 4: Establish more robust methods for estimating non-tuition costs

Half of all undergraduates (50 percent) live off campus, while the remainder live on campus or at home.10 When providing financial aid, colleges are required to estimate living costs for students who are living on their own. However, estimating off campus housing costs can be challenging, resulting in dramatic variation of estimates of off-campus living costs among colleges, even between colleges in the same city. Researchers have found, for example, that college estimates of living costs in Washington, DC ranged from $9,387 to $20,342, while colleges in Milwaukee have estimated costs ranging from $5,180 to $21,276.11 Furthermore, researchers have estimated that one-third of colleges underestimate living expenses.12 The estimation of living costs has critical implications for students who depend on financial aid. Underestimationof living expenses can mean insufficient financial aid; overestimation can lead to students borrowing more money than they need.

Many schools survey students to obtain information on living costs. These surveys do not accurately estimate costs, because they capture what students are spending as opposed to what they need to spend.13 Under-resourced students may underreport costs, because they are missing meals, sleeping in their cars, or couch surfing.14 A survey of undergraduates at the University of California, Berkeley found that 23 percent of students reported skipping meals at least somewhat often to save money.15 On the other hand, wealthier students may report higher living costs than necessary.16

When estimating off-campus living expenses, schools should use standardized information or validate student-reported information with standardized data, such as data from the U.S. Department of Housing and Urban Development, U.S. Department of Agriculture Food Plans, and the U.S. Bureau of Labor Statistics. The significance of this information is too important to get wrong.

Strategy 5: Educate students about financial aid

Relatively few students have even minimal knowledge about financial aid. According to the 2015 Administrative Budget Survey, administered by the National Association of Student Financial Aid Administrators (NASFAA), over 70 percent of administrators at four-year institutions reported that students’ financial literacy was “limited.”17 Knowing the source and requirements of financial aid enables students to make better financial planning decisions.

Schools should encourage or require students to meet with a financial aid adviser before signing off on financial aid packages to ensure students understand their packages and make informed financial decisions. One study of financial aid recipients found that when students sought financial aid advising, they found it useful.18 Alternatively, schools should also offer webinars or videos that walk students through an example of a financial aid letter and discuss common questions or issues that students face to help them better understand their financial aid packages.

Some processes that ostensibly help facilitate approval of grants are problematic. For example, there are online systems that allow students to sign off on their financial aid packages without fully examining or understanding them. Further, a student’s parent may independently agree to a financial aid package if a student has consented to allow their parents access to their financial aid information. Parents should not be allowed to consent to burdens imposed on their children.

Examples of Financial Aid Educational Resources Offered by Schools

- Stony Brook University (SUNY)

Financial aid YouTube page covering a range of topics, including “Accept and Decline Aid” and “SBU Satisfactory Academic Progress Guidelines.” - University of California at Berkeley

YouTube page offers videos addressing various financial aid topics. Videos include a tutorial of UC Berkeley’s financial aid system. - University of Wisconsin-Milwaukee

Presentations for students and parents.

Easing the Financial Burden

As noted, rising college costs can make higher education seemingly unattainable for low-income students. They are more likely to forgo higher education entirely due to perceived financial constraints.19 It is no surprise that low-income families are more likely to find financial assistance critical in selecting a college, particularly in light of the high price of a college education.20 These students’ college choices may be limited to what they can afford rather than the best fit. For high performing, low-income students, this may mean sacrificing selectivity.

Once enrolled in college, low-income students are more likely to leave without obtaining a degree. Insufficient funds to meet basic needs and the requirement to work while in school contribute to the increased rate of attrition.21

Schools can help to ease the burden of financial stress and support low-income students in multiple ways, outlined in strategies 6 through 9 below.

Strategy 6: Prioritize need-based institutional grants

Over the last 20 years there has been a shift towards merit-based scholarships and away from need-based aid. In 1995, the majority of institutional award dollars were need-based.²² However, by 2003 the majority of institutional award dollars were merit-based.

Non-need-based aid, such as merit scholarships, is likely to attract students who can afford to pay for college. It also attracts students who are at the top of their class.²³ Accordingly, merit-based awards benefit institutions, but they can exacerbate the excellence gap by limiting aid to students who may need it the most.

In other words, wealthier students may be getting more aid than they need, while low-income students are unable to meet even their minimum financial requirements. A study by Postsecondary Education Opportunity suggests that students from lower-income families had greater unmet need than their higher income peers.²⁴ Another study found that more than a quarter of students from the top income quartile, or students from families that can afford to pay for college, received merit grants.²⁵ Accordingly, institutional aid that is used for merit aid hurts low-income students while not materially helping wealthier students as they have little to no financial need.

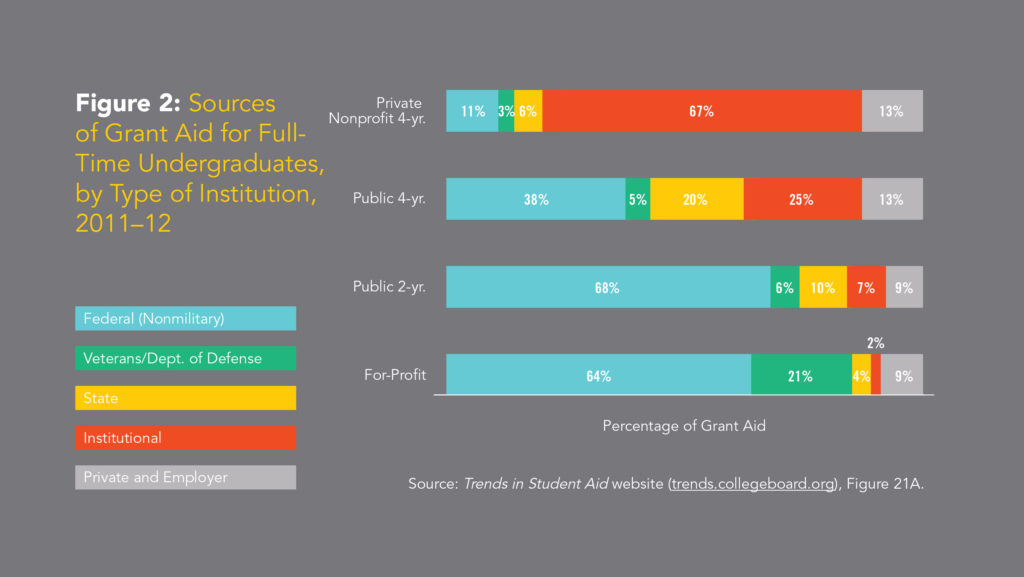

Institutional aid is an important source of financial aid, particularly among students attending private institutions (see Figure 2). In 2011–12, 67% of the aid received by students attending private four-year colleges came from institutional grants, and 25% of the aid received by students at public four-year colleges came from institutional grants.²⁶

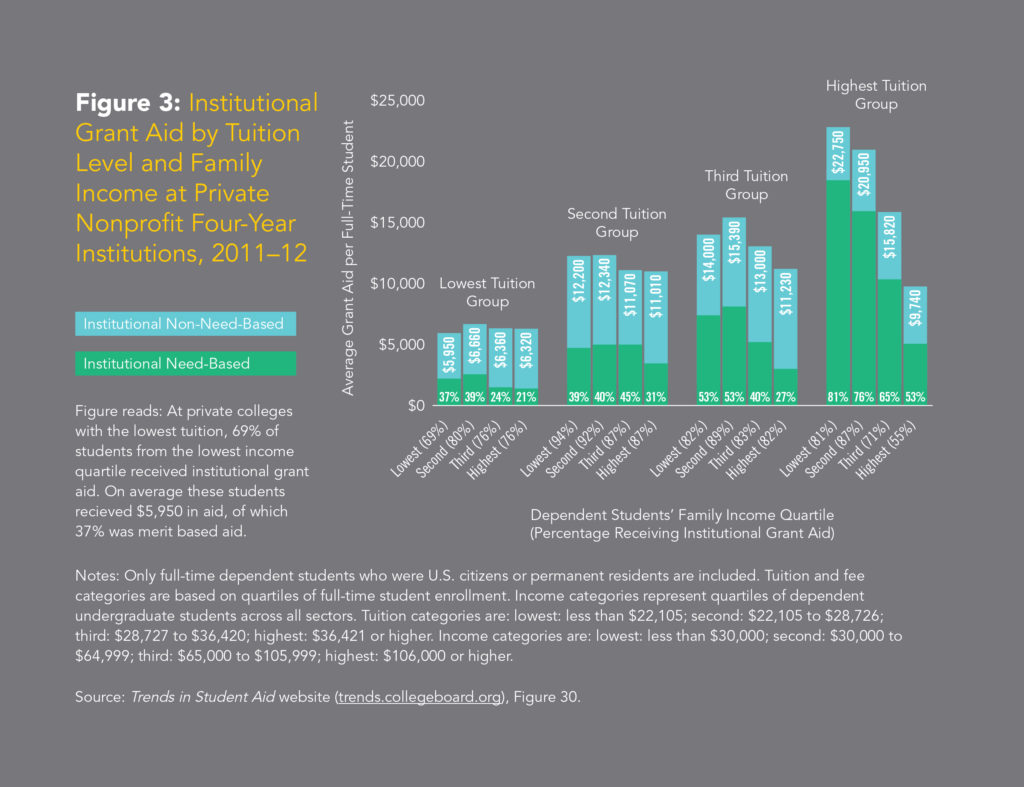

Closer examination of private colleges and universities shows varying practices in institutional aid. At the lowest-priced private institutions, low-income students actually receive less institutional aid than students from higher-income families, because of the merit aid awarded to high-income students. Unsurprisingly, at the highest-priced institutions, low-income

students, on average, receive almost double the institutional aid than students from the highest income quartile (see Figure 3).²⁷

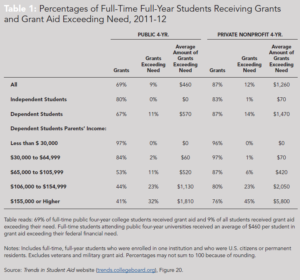

Additionally, high-income students are significantly more likely to obtain funding that exceeds their need (see Table 1).²⁸ Students in the highest-income bracket attending private four-year institutions received an average of $5,800 in aid exceeding their need. Almost half (45 percent) of students from the highest-income brackets that attended private institutions received grant aid beyond what their need dictates.

Figure 2: Sources of Grant Aid for Full-Time Undergraduates,by Type of Institution, 2011–12

Figure 3: Institutional Grant Aid by Tuition Level and Family Income at Private Nonprofit Four-Year Institutions, 2011–12

Table 1: Percentages of Full-Time Full-Year Students Receiving Grants and Grant Aid Exceeding Need, 2011-12

Strategy 7: Commit to maintaining grant levels for the duration of a student’s academic program

Students entering college may assume that grant funds will be stable throughout their college years. However, research indicates that institutional grant aid at private universities decreases by an average of $1,000 between freshman and senior year.²⁹ Just as unexpected tuition increases can derail students,³⁰ unexpected losses in grant funds can potentially interfere with a student’s educational progress, particularly when loss of grants are coupled with increases in tuition and fees. Schools should seek to maintain grant funds throughout the course of a student’s academic program, provided the student maintains minimum academic standards.

–Examples of Schools Committed to Maintaining Institutional Grant Levels for Four Years*

*Grants may be contingent on yearly application and changes in need

–Examples of Schools Offering Need-Based Grants Only

- Vassar College

- Stanford University

- Harvard University

- Northwestern University

- Franklin and Marshall College

Strategy 8: Do not reduce institutional aid when students receive private scholarships

Private scholarships can help students meet unmet need and reduce debt. Many students seek such scholarships to make college more affordable and to avoid taking loans. However, displacement of institutional aid undermines the purpose of private scholarships as the net price is not decreased and college does not become more affordable. In a survey of their scholarship recipients, the Dell Scholars program found that 60 percent of scholarship recipients were adversely affected by award displacement.³¹ When schools engage in displacement, they limit the benefit of private scholarships, particularly for low-income students. Scholarships should supplement institutional aid, rather than supplant it.

– Examples of Schools with a Policy of Reducing Loans and/or Work Study Before Institutional Grants

Strategy 9: Utilize low-cost textbooks

The cost of academic materials such as textbooks may place a burden on students with unmet financial need. The average cost of textbooks has increased by 73 percent over the past decade, and an individual textbook can cost over $200.³² With nearly all courses requiring a textbook,³³ these materials can add up quickly. Students may be forced to go without textbooks or purchase textbooks and make other sacrifices in return.

A study by the Lumina Foundation found that most instructors do consider the cost of textbooks when choosing course materials for their students.³⁴ Furthermore, faculty tend to be dissatisfied with the high cost of texts. One faculty member from the study is quoted as saying, “At a time when we are concerned about the cost of a university education and student debt, a $246 text is obscene.” Open-licensed educational materials or open textbooks can significantly reduce course material costs. Yet, the awareness of these alternative resources among faculty tends to be low.³⁵

The U.S. Public Interest Research Group (U.S. PIRG) argues that institutions are well equipped to address the issue of textbook prices through their libraries and support staff. They suggest a number of ways that schools can encourage the use of openly licensed materials.³⁶ Their recommendations include:

- Expand open textbook use on campus. Currently only five percent of courses use an openly licensedrequired textbook.³⁷

- Implement policies that demonstrate administrative support of, but do not mandate, open textbooks as a possible choice for course materials.

- Develop programs that provide training and coaching around the use of open textbooks.

- Offer faculty release time or stipends to explore open materials and incorporate them into their courses.

- Assign a chair or committee with the coordination of these efforts.

–Examples of Schools Providing Information About Open Education Resources